In the dynamic world of corporate governance and regulatory compliance, staying informed is essential. We bring to your attention a series of noteworthy legal and regulatory changes that could significantly impact how businesses operate, strategize, and grow. These developments underscore the government’s push toward greater transparency, accountability, and ease of doing business in India. In this edition, we break down the most relevant updates, offering practical insights to help you remain compliant and ahead of the curve.

CORPORATE COMPLIANCE

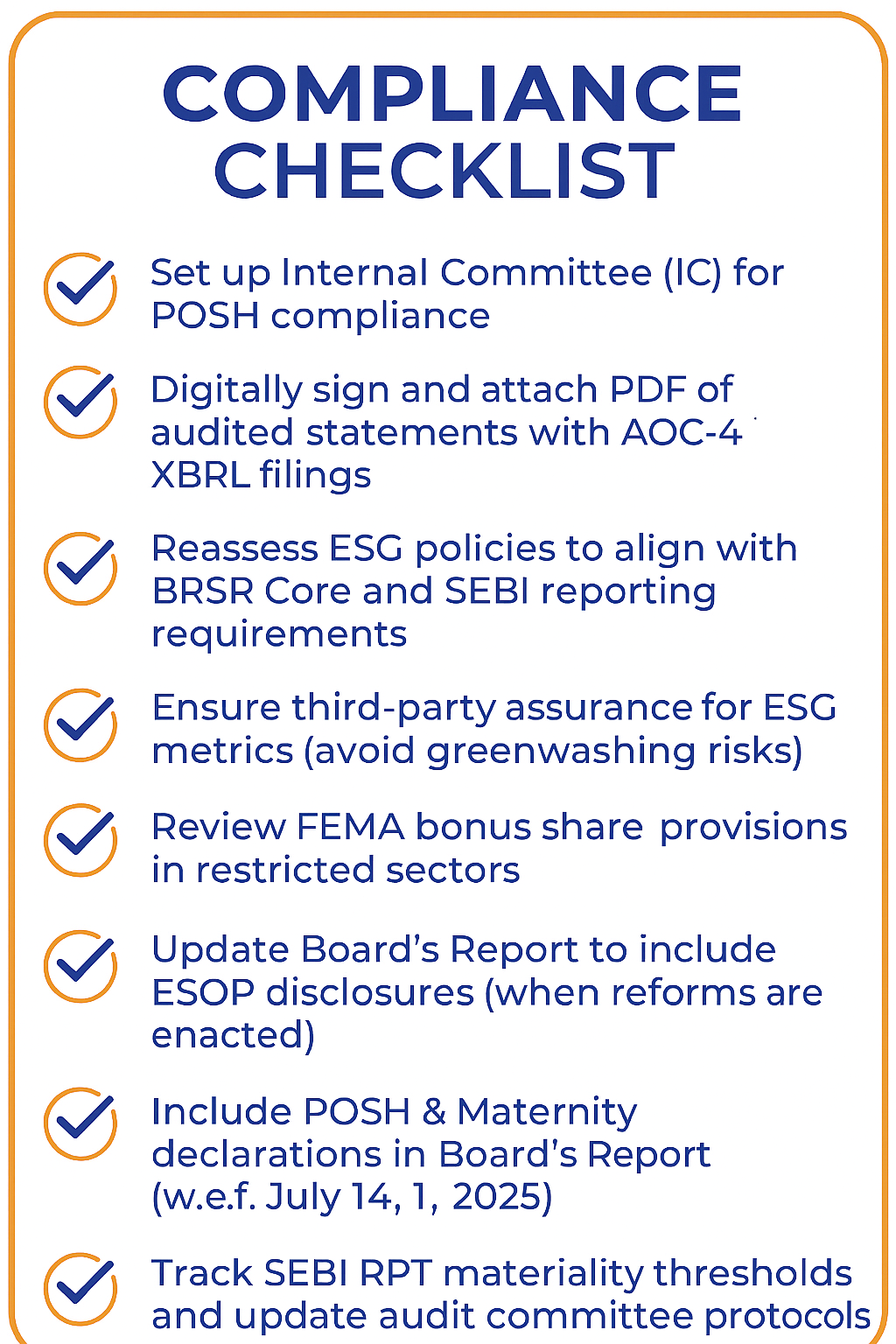

1. New MCA Disclosure Mandates on POSH and Maternity Compliance

(Effective: July 14, 2025)

The Ministry of Corporate Affairs (MCA), vide its Companies (Accounts) Second Amendment Rules, 2025 (G.S.R. 357(E) dated May 30, 2025), has introduced significant changes requiring mandatory disclosure of workplace safety and maternity benefits data in the Board’s Report. This transformative shift underscores the government’s commitment to gender-sensitive governance and enhanced corporate accountability.

Key Mandates:

Annual Data on Sexual Harassment Complaints: Companies are now obligated to provide granular data in their Board’s Report, as per Rule 8(5)(x) of the Companies (Accounts) Rules, 2014, as amended by the 2025 Rules. This includes:

- Number of complaints received under the Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 (POSH Act) received during the financial year.

- Number of complaints disposed of during the financial year.

- Number of cases pending beyond a period of ninety days.

An unequivocal declaration of compliance with the provisions relating to the constitution of the Internal Committee (IC) under the POSH Act.

Maternity Benefit Act Compliance: Rule 8(5)(xiii) of the Companies (Accounts) Rules, 2014, as inserted by the 2025 Rules, mandates companies to include a statement confirming compliance with the Maternity Benefit Act, 1961, including provisions for 26 weeks of paid leave, nursing breaks, and creche facilities where applicable. Companies must formally assess the applicability of these provisions, and if not applicable (e.g., due to employee thresholds), such exemption must be expressly stated.

Legal Provisions:

- Section 134 of the Companies Act, 2013, read with Rule 8 of the Companies (Accounts) Rules, 2014, as amended by the Companies (Accounts) Second Amendment Rules, 2025.

- Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013.

- Maternity Benefit Act, 1961.

Implications: This move brings previously internal matters into the realm of audited statutory disclosures, significantly raising reputational and regulatory stakes. Companies must ensure their Internal Committees (ICs) under the POSH Act are correctly constituted, trained regularly, and operationally active. The change also mandates digital filing under MCA V3, which will be closely scrutinized by auditors and regulators. Non-compliance can trigger penal action under Section 134(8) of the Companies Act, 2013, which imposes penalties on the company and every officer in default.

Relevant Notification:

G.S.R. 357(E) dated May 30, 2025, notifying the Companies (Accounts) Second Amendment Rules, 2025.

2. Digitally Signed PDF Mandate with AOC-4 XBRL Filings

(Effective: July 14, 2025)

In a strong push towards digital and uniform compliance, the MCA has mandated that all companies filing AOC-4 XBRL must now attach a digitally signed PDF copy of the audited financial statements. This is part of a broader migration to the MCA V3 portal for e-filing of 38 forms, effective from July 14, 2025.

Key Mandates:

Mandatory Attachment: As per the Companies (Filing of Documents and Forms in Extensible Business Reporting Language) Amendment Rules, 2025 (G.S.R 371(E) dated June 6, 2025), companies filing Form AOC-4 XBRL must attach a duly authenticated PDF copy of their signed financial statements. This includes:

- Director’s Report (as per Section 134(3) of the Companies Act, 2013)

- Auditor’s Report (as per Section 143 of the Companies Act, 2013)

- Notes to Accounts

Digital Signature Synchronization: Companies must ensure that digital signatures are synchronized and all versions of the financial statements (XBRL data and human-readable PDF) are harmonized.

Rejection for Non-Compliance: The MCA system will automatically reject submissions with missing, unsigned, or mismatched PDFs.

Legal Provisions:

- Section 137 of the Companies Act, 2013 (Filing of financial statements).

- Rule 12 of the Companies (Accounts) Rules, 2014, as amended by the Companies (Accounts) Second Amendment Rules, 2025 (inserting new sub-rule (1C) for mandatory e-forms containing extracts of Board’s Report and Auditor’s Reports).

- Companies (Filing of Documents and Forms in Extensible Business Reporting Language) Amendment Rules, 2025.

Implications: This reform targets quality assurance in financial reporting and aims to prevent discrepancies between XBRL data and human-readable reports. It has implications not only for ROC compliance but also for due diligence exercises, investor assessments, and public disclosure integrity.

Relevant Notification:

G.S.R 371(E) dated June 6, 2025, notifying the Companies (Filing of Documents and Forms in Extensible Business Reporting Language) Amendment Rules, 2025.

STARTUPS

3. Proposed Reforms in ESOP Disclosures and Taxation for Unlisted Companies

The government is actively considering reforms to ease taxation and enhance transparency of Employee Stock Option Plans (ESOPs), particularly for startups and unlisted companies. These proposed measures aim to make ESOPs a more attractive tool for talent retention and startup growth.

Proposed Measures (subject to legislative changes):

Deferred Taxation until Share Sale or Liquidity Event: This is a crucial reform being discussed. Currently, perquisite tax on ESOPs for employees of unlisted companies is often triggered at the time of exercise, even if there’s no immediate liquidity event. The proposal is to defer this taxation until the shares are sold, the employee leaves the company, or after a specified period (e.g., five years from allotment), whichever is earliest. This aligns with the existing tax deferral option for eligible startups holding an Inter-Ministerial Board (IMB) Certificate, as per Section 17(2)(vi) of the Income Tax Act, 1961, read with Rule 3(8) of the Income Tax Rules, 1962, and Section 80IAC of the Income Tax Act, 1961. The proposed reform seeks to extend this benefit more broadly to unlisted companies.

Mandatory Board Report Disclosure of ESOP Grant Details and Accounting Treatment: While not explicitly mandated for unlisted companies under the Companies Act for specific ESOP details (unlike for listed companies under SEBI (Share Based Employee Benefits & Sweat Equity) Regulations, 2021), the proposed reform suggests making such disclosures mandatory in the Board’s Report. This would enhance transparency and provide stakeholders with a clearer picture of the company’s ESOP schemes. This would likely be introduced as an amendment to Rule 8 of the Companies (Accounts) Rules, 2014, or through specific notifications.

Alignment of Valuation Norms with Income Tax and FEMA Rules: The valuation of unlisted shares for ESOP purposes can be complex, often requiring different methodologies under the Income Tax Act, FEMA (Foreign Exchange Management Act) regulations, and the Companies Act. The proposal aims to harmonize these valuation norms to reduce ambiguity and compliance burden.

Legal Framework (Existing & Potential Amendments):

- Companies Act, 2013: Primarily Section 62(1)(b) and Rule 12 of the Companies (Share Capital and Debentures) Rules, 2014, govern the issuance of ESOPs by unlisted companies.

- Income Tax Act, 1961: Section 17(2)(vi) deals with ESOPs as perquisites, and Section 112A and Section 111.

- Foreign Exchange Management Act, 1999 (FEMA) and relevant regulations (e.g., Foreign Exchange Management (Non-debt Instruments) Rules, 2019) for valuation in cross-border ESOPs.

Implications: These reforms, if enacted, would significantly alleviate the tax burden on employees of unlisted companies and provide greater clarity and consistency in ESOP management, making them a more effective tool for attracting and retaining talent in the growing startup ecosystem.

ESG

4. SEBI’s Strengthened Corporate Governance Norms for Listed Companies (LODR Amendment)

Recent amendments to the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (LODR Regulations), are bringing increased rigor to corporate governance frameworks for listed companies, especially for Small and Medium Enterprises (SMEs) and High-Value Debt Listed Entities (HVDLEs). These measures are designed to boost investor confidence, standardize disclosures, and enforce greater board accountability.

Key Changes and Provisions:

Mandatory Disclosure of ESG Metrics through BRSR Core:

Legal Provision: Regulation 34(2)(f) of the SEBI (LODR) Regulations, 2015, mandates the submission of the Business Responsibility and Sustainability Report (BRSR). The BRSR Core, a more focused set of KPIs, is applicable to the top 1000 listed entities by market capitalization, starting from FY 2023-24, as per SEBI Circular SEBI/HO/CFD/CFD-SEC-2/P/CIR/2023/122 dated July 12, 2023.

Implication: This requires companies to provide assured data on key environmental, social, and governance aspects, enhancing transparency and accountability.

Enhanced Scrutiny and Approval Process for Related Party Transactions (RPTs):

Legal Provision: Regulation 23 of the SEBI (LODR) Regulations, 2015, governs RPTs. Recent amendments (e.g., through SEBI (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2025, notified on March 27, 2025, effective April 1, 2025, for SME-listed entities exceeding certain thresholds) have strengthened the requirement for audit committee and, in some cases, shareholder approval for material RPTs. The definition of materiality for RPTs for SME-listed entities has also been revised (e.g., exceeding INR 50 crore or 10% of annual consolidated turnover, whichever is lower, from April 1, 2025).

Implication: This aims to prevent transactions that could be detrimental to minority shareholders’ interests and ensures greater transparency.

Mandatory External Board Evaluation:

Legal Provision: While a specific general circular for “external” board evaluation for all top 1000 listed entities isn’t explicitly linked to a single, recent circular, the broader corporate governance framework under Regulation 17 (Board of Directors) and Schedule II of the SEBI (LODR) Regulations, 2015, emphasizes robust performance evaluation mechanisms for the board, committees, and individual directors. SEBI has been consistently pushing for more objective and independent evaluation. The SEBI (LODR) (Amendment) Regulations, 2025 (notified on March 27, 2025) have introduced governance norms for HVDLEs, which include detailed requirements for board composition, meetings, and the role of independent directors in enhancing board effectiveness.

Implication: This promotes objective assessment of board effectiveness and helps identify areas for improvement in governance.

Periodic Review of Policies by Nomination and Remuneration Committees (NRC):

Legal Provision: Regulation 19 of the SEBI (LODR) Regulations, 2015, mandates the constitution and functions of the NRC. The NRC is responsible for formulating the criteria for determining qualifications, positive attributes, and independence of a director and recommending to the board a policy relating to the remuneration of directors, key managerial personnel, and senior management. The emphasis on ‘periodic review’ ensures these policies remain relevant and effective.

Implication: This reinforces the role of the NRC in ensuring a competent and well-governed board and fair remuneration practices.

Relevant Notifications:

- SEBI (Listing Obligations and Disclosure Requirements) (Amendment) Regulations, 2025 – Notification No. F. No. SEBI/LAD-NRO/GN/2025/239 dated March 27, 2025.

- SEBI Circular SEBI/HO/CFD/CFD-SEC-2/P/CIR/2023/122 dated July 12, 2023 on BRSR Core.

Implication: Listed companies must revisit their compliance calendars, internal controls, and audit committee charters to ensure alignment with SEBI’s expectations. Non-compliance with LODR Regulations can lead to significant penalties, including fines and suspension of trading of securities.

5. SEBI’s Crackdown on Greenwashing: ESG Claims under the Scanner

As ESG investing grows, SEBI is clamping down on false or exaggerated sustainability claims, a practice known as “greenwashing.” This intensified scrutiny applies to green claims made in investor presentations, IPO documents, CSR Reports, and other public disclosures.

Key Expectations and Provisions:

Substantiation of Data with Third-Party Audits:

Legal Basis: While there isn’t one single “greenwashing” regulation, SEBI leverages its powers under the SEBI Act, 1992, and the SEBI (LODR) Regulations, 2015, to ensure fair and accurate disclosures. The BRSR Core framework, particularly with its phased assurance requirements, implicitly demands third-party validation for reported ESG data. For instance, the SEBI Circular SEBI/HO/CFD/CFD-SEC-2/P/CIR/2023/122 dated July 12, 2023[1], mandates limited assurance for select KPIs from FY 2023-24, moving to reasonable assurance from FY 2026-27.

Implication: Generic or unverifiable claims are no longer acceptable. Companies must back up their sustainability assertions with verifiable data and, where applicable, external certifications (e.g., ISO standards, carbon audits).

Strict Adherence to BRSR Reporting Standards:

Legal Basis: Regulation 34(2)(f) of LODR read with the SEBI/HO/CFD/CFD-SEC-2/P/CIR/2023/122 dated July 12, 2023, explicitly outlines the BRSR Core reporting requirements.

Implication: Companies must follow the prescribed formats and ensure comprehensive and accurate reporting, avoiding selective disclosures.

Avoid Selective or Misleading Disclosures:

Legal Basis: This aligns with the fundamental principles of Regulation 4 of LODR (General obligations of listed entities) and the overarching objective of investor protection under the SEBI Act, 1992. Misleading statements in offer documents could also attract provisions of the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

Implication: Transparency is paramount. Companies must provide a balanced view of their ESG performance, including progress and challenges.

Penalties and Enforcement:

Greenwashing carries tangible legal and reputational risks, including:

- Monetary fines: Under Section 15HA of the SEBI Act, 1992 (for fraudulent or unfair trade practices related to the securities market).

- Suspension of public fundraising: IPOs or Qualified Institutional Placements (QIPs) will be suspended if disclosures in offer documents are found to be misleading.

- Litigation risks from investors, NGOs, or regulators for misrepresentation.

- Negative ESG ratings will affect index inclusion and institutional investor interest.

Regulatory Framework for ESG Rating Agencies and Assurance Providers:

Legal Provision: SEBI has already rolled out a regulatory framework for ESG Rating Providers (ERPs) through a Master Circular for ESG Rating Providers (SEBI/HO/DDHS/POD2/P/CIR/2023/121 dated July 12, 2023), under the SEBI (Credit Rating Agencies) Regulations, 1999. While registration is currently voluntary, it sets out obligations for transparency of methodologies and avoidance of conflicts of interest.

Implication: This framework aims to bring greater standardization and credibility to ESG ratings, further curbing potential greenwashing. SEBI is expected to continue strengthening oversight over assurance providers as well.

RBI, FEMA AND CROSS BORDER M&A

6. FEMA Rule Relaxation: Bonus Shares Now Allowed in FDI Prohibited Sectors

The Ministry of Finance, Department of Economic Affairs, has provided long-awaited relief to foreign-owned businesses operating in sectors where Foreign Direct Investment (FDI) is prohibited. The Foreign Exchange Management (Non-Debt Instruments) (Amendment) Rules, 2025 now permit Indian companies in such sectors to issue bonus shares to their existing non-resident shareholders.

Key Provisions and Conditions:

Legal Basis: The amendment has been introduced via Sub-rule (2) under Rule 7 of the Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (NDI Rules). This amendment was reportedly notified on June 11, 2025, following a Press Note from the Department for Promotion of Industry and Internal Trade (DPIIT) in April 2025.

Permissible Sectors: This applies to sectors where fresh FDI is prohibited, such as lottery business, gambling and betting, chit funds, Nidhi companies, real estate business (excluding construction of townships, etc.), and manufacturing of cigars, cheroots, cigarillos, and cigarettes, as outlined in Paragraph 2 of Schedule I of the NDI Rules and Paragraph 5.1 of the Consolidated FDI Policy Circular.

Conditions for Issuance: The issuance of bonus shares is permitted only if:

- The ownership percentage of the non-resident shareholders remains unchanged post-issuance. This means the bonus issue must be proportional to existing shareholdings.

- No fresh capital inflow occurs.

- No new control rights are created in violation of sectoral caps or FDI policy.

Retrospective Regularization: The amendment also provides for retrospective regularization of past bonus share issuances made during regulatory “grey periods,” offering immense relief to companies previously exposed to FEMA non-compliance.

Relevant Notification:

Foreign Exchange Management (Non-Debt Instruments) (Amendment) Rules, 2025, notified on June 11, 2025

Implications: This relaxation helps foreign joint ventures and subsidiaries reinforce capital structures and reward existing foreign shareholders without violating sectoral caps or attracting fresh FDI restrictions. Companies must ensure meticulous legal documentation, obtain necessary shareholder approvals, and validate historical cap tables to avoid triggering FDI reclassification and penal consequences under FEMA, 1999.

7. Fast Track Merger Regime under Section 233: A Boon for Internal Restructuring

The Ministry of Corporate Affairs (MCA) has continued to fine-tune the fast-track merger regime under Section 233 of the Companies Act, 2013, encouraging group-level consolidation and simplification of corporate structures. This regime enables qualifying mergers without the lengthy National Company Law Tribunal (NCLT) involvement.

Key Provisions and Recent Enhancements:

Legal Basis: Section 233 of the Companies Act, 2013, read with Rule 25 of the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016.

Eligible Companies: The fast-track merger route is available for:

- Holding company and its wholly-owned subsidiary company.

- Two or more small companies.

- Two or more start-up companies.

- One or more start-up companies with one or more small companies.

Proposed Expansion: As per recent discussions (e.g., Union Budget 2025-26 discussions), the MCA has proposed to widen the scope further to include:

Inclusion of Financially Sound Unlisted Companies

- Eligibility Criteria: Unlisted companies (other than Section 8 companies) with borrowings less than ₹50 crore, no defaults on repayments, and an auditor’s certificate confirming eligibility.

Flexible Merging for Holding Companies and Subsidiaries

- Current Rule: Only wholly-owned subsidiaries can merge with their holding companies under Section 233(1)(b).

- Proposed Change: Holding companies—whether listed or unlisted—will be allowed to merge with one or more unlisted subsidiaries even if it holds less than 100% shares of the unlisted subsidiary.

Merging of Sibling Subsidiaries

- Current Rule: Subsidiaries under the same parent cannot merge through the fast-track route.

- Proposed Change: Unlisted subsidiary companies that share the same holding company will now be eligible to merge via the fast-track process.

Integration of Foreign Holding Company Mergers

- Current Handling: Mergers between a foreign holding company and its Indian wholly-owned subsidiary are managed under Rule 25A(5).

- Proposed Change: These mergers will be incorporated into Rule 25 which deals with mergers between Indian companies and foreign companies.

Benefits:

- Fewer procedural formalities compared to the NCLT route (Sections 230-232).

- Quicker approval from the Regional Director (RD) and Registrar of Companies (ROC).

- Exemption from shareholder meetings in some cases (e.g., if approved by 90% in value of shareholders in a holding-subsidiary merger).

- Significant legal cost savings.

Relevant Notifications:

- Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 (Original rules).

- Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2024, effective September 17, 2024 (for cross-border fast-track mergers).

- Draft Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2025, circulated for public comments in April 2025, proposing to expand the scope to unlisted companies (Final notification is awaited).

Implications: The regime is gaining popularity among corporate groups aiming to reduce dormant entities, achieve tax efficiency, and streamline holding structures. However, meticulous documentation, adherence to threshold criteria, and compliance with all prescribed procedures remain essential to ensure valid mergers and avoid future disputes.

For comprehensive details, refer to the following documents:

Public Notice: MCA Public Notice– https://www.mca.gov.in/bin/dms/getdocument?mds=Vl7V8BHbA7gmKAjfxzhiTw%253D%253D&type=open

Draft Notification: MCA Draft Notification– https://www.mca.gov.in/bin/dms/getdocument?mds=KlrEic%252FleYvKv6dibvt8HQ%253D%253D&type=open

8. RBI Clarifications on Deferred Consideration in Cross-Border M&A

Cross-border Merger and Acquisition (M&A) transactions involving deferred consideration (such as holdbacks, escrow arrangements, and milestone-based payments) have received specific regulatory attention from the Reserve Bank of India (RBI). These clarifications aim to provide certainty while ensuring compliance with foreign exchange regulations.

Key Clarifications and Provisions:

- Legal Basis: These guidelines are typically issued under the Foreign Exchange Management Act, 1999 (FEMA), and the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019 (NDI Rules). The RBI’s Master Direction on Foreign Investment in India (updated periodically, e.g., in January 2025) often consolidates such clarifications.

- Limits for Automatic Route: The RBI has permitted deferment of up to 25% of the total consideration for a maximum period of 18 months from the date of the transfer agreement, without prior RBI approval. This applies to both resident to non-resident and non-resident to resident share transfers.

- Prior RBI Approval Required:

- Deferred payments exceeding 25% of the total consideration.

- Payments extending beyond 18 months from the date of the transfer agreement.

- Documentation and Reporting:

- The timeline and quantum of deferred payouts must be explicitly captured in transaction documents.

- These payments must be reported via Form FC-TRC (Foreign Currency-Transfer of Shares) or Form FC-GPR (Foreign Currency-Gross Provisional Return) as applicable, along with the other transaction details.

- Applicability to Downstream Investments: Recent clarifications in the updated Master Direction on Foreign Investment in India (January 2025) have explicitly stated that deferred consideration arrangements (including share swaps) available for foreign direct investment are also available for downstream investments made by Foreign Owned and Controlled Companies (FOCCs) in other Indian entities, subject to adherence to Rule 23 of the NDI Rules (e.g., funding through foreign inward remittance or internal accruals).

Relevant Circulars / Master Directions:

- Foreign Exchange Management (Non-Debt Instruments) Rules, 2019.

- RBI Master Direction on Foreign Investment in India, updated periodically. (The January 2025 update is particularly relevant for the downstream investment clarification).

- P. (DIR Series) Circular No. 67 dated May 20, 2016 was a significant circular initially allowing the 25%/18-month deferment without prior RBI approval.

Implications: These clarifications are crucial for deal structuring in private equity exits, strategic acquisitions, and international joint ventures. Legal teams must factor in RBI timelines and approval requirements to avoid post-deal bottlenecks, penalties under FEMA, 1999, and compliance delays. Careful drafting of transaction documents to align with these rules is essential.

[1] https://ca2013.com/wp-content/uploads/2023/07/SEBI-Circular_12.07.2023.pdf